Summary of Cooling Measures Affecting Buyers

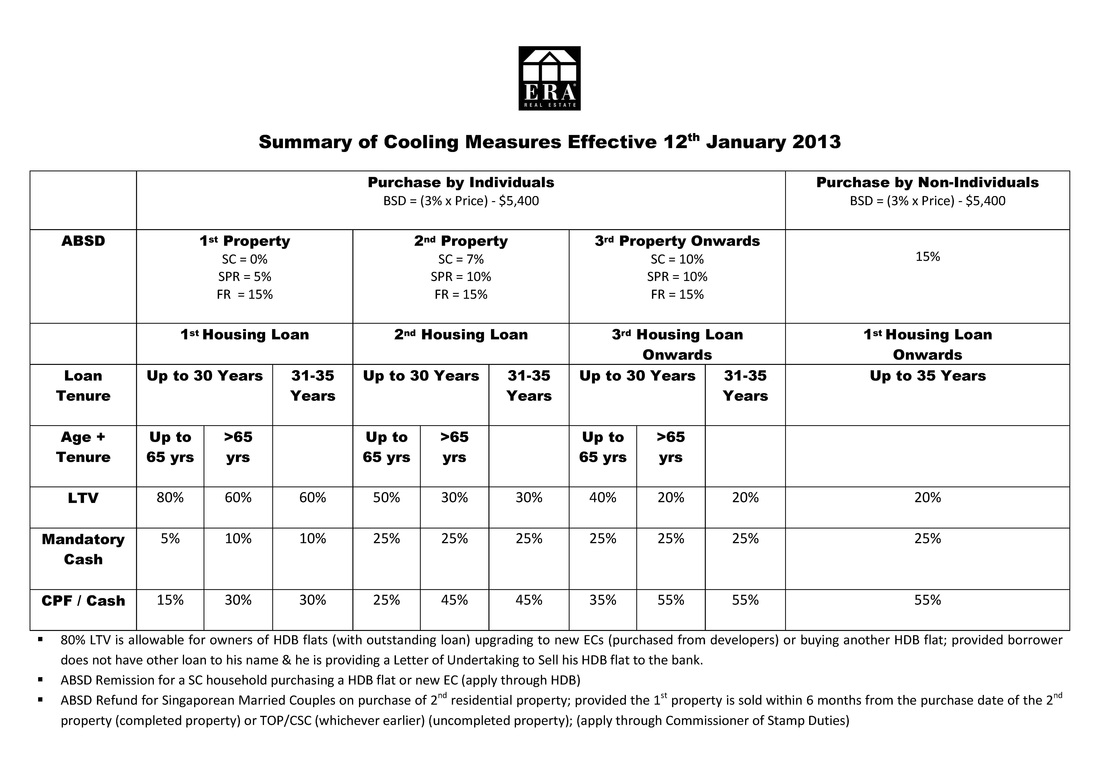

Buyer Stamp Duty (BSD)

Anybody buying a residential property in Singapore is required to pay a Buyer Stamp Duty (BSD) equivalent to roughly 3% of the purchase price or valuation price, whichever is higher.

Additional Buyer Stamp Duty (ABSD)

To cool the market, the government introduced an Additional Buyer Stamp Duty (the ABSD) which varies according to your immigration status

Exemptions and Reliefs:

• Nationals from the USA, Switzerland, Norway, Iceland, and Liechtenstein are exempted from paying the ABSD for foreigners. The ABSD rule applying to them is the same than Singapore citizens.

• Married couples with at least 1 Singapore citizen will be exempted from paying the ABSD if:

- None of them already owns a property;

- They agree to dispose of their existing property within 6 months of the purchase of their new property (or the TOP if the new property is uncompleted).

Loan Tenure limit

Tenures of loans granted by financial institutions regulated by the MAS are limited to 35 years.

Loan-To-Value (LTV) limits

The LTV limit is the maximum percentage of the purchase price or valuation price (given by the bank), whichever is lower, that can be borrowed from the bank.

Exemptions and Reliefs: If you own a residential property in Singapore, you are not subject to these limits when you obtain a housing loan for the purchase of a property which is an Executive Condominium (EC) purchased directly from a property developer or a HDB flat (which requires you to dispose of your previous flat)

Minimum Cash Down Payment (Mandatory Cash)

There is a minimum percentage of the purchase price or valuation price, whichever is lower, that has to be paid in cash (Mandatory Cash).

Central Provident Fund (CPF) / Cash

The remaining amount (from the LTV) that cannot be borrowed from the bank has to be paid in cash or can come from a CPF ordinary account (mandatory saving account for Singapore citizens and Permanent Residents).

Total Debt Servicing Ratio (TDSR)

The Total Debt Servicing Ratio framework is a set of rules that restrict financial institutions from lending to an individual if his outstanding debt repayments (any debt including non-related property) exceed 60% of his gross income (including the potential new loan). The interest rate used for calculation of the new loan is 3.5% or the actual interest rate, whichever is higher.

Anybody buying a residential property in Singapore is required to pay a Buyer Stamp Duty (BSD) equivalent to roughly 3% of the purchase price or valuation price, whichever is higher.

Additional Buyer Stamp Duty (ABSD)

To cool the market, the government introduced an Additional Buyer Stamp Duty (the ABSD) which varies according to your immigration status

Exemptions and Reliefs:

• Nationals from the USA, Switzerland, Norway, Iceland, and Liechtenstein are exempted from paying the ABSD for foreigners. The ABSD rule applying to them is the same than Singapore citizens.

• Married couples with at least 1 Singapore citizen will be exempted from paying the ABSD if:

- None of them already owns a property;

- They agree to dispose of their existing property within 6 months of the purchase of their new property (or the TOP if the new property is uncompleted).

Loan Tenure limit

Tenures of loans granted by financial institutions regulated by the MAS are limited to 35 years.

Loan-To-Value (LTV) limits

The LTV limit is the maximum percentage of the purchase price or valuation price (given by the bank), whichever is lower, that can be borrowed from the bank.

Exemptions and Reliefs: If you own a residential property in Singapore, you are not subject to these limits when you obtain a housing loan for the purchase of a property which is an Executive Condominium (EC) purchased directly from a property developer or a HDB flat (which requires you to dispose of your previous flat)

Minimum Cash Down Payment (Mandatory Cash)

There is a minimum percentage of the purchase price or valuation price, whichever is lower, that has to be paid in cash (Mandatory Cash).

Central Provident Fund (CPF) / Cash

The remaining amount (from the LTV) that cannot be borrowed from the bank has to be paid in cash or can come from a CPF ordinary account (mandatory saving account for Singapore citizens and Permanent Residents).

Total Debt Servicing Ratio (TDSR)

The Total Debt Servicing Ratio framework is a set of rules that restrict financial institutions from lending to an individual if his outstanding debt repayments (any debt including non-related property) exceed 60% of his gross income (including the potential new loan). The interest rate used for calculation of the new loan is 3.5% or the actual interest rate, whichever is higher.

Back to Useful Information